Topps Group operates in the highly fragmented UK tile market, serving both the domestic repair, maintenance and improvement (‘RMI’) sector and commercial segments including housebuilders and infrastructure.

Market Opportunity

The UK tile market is valued at around £700 million annually. No single distributor holds a dominant share, creating an attractive environment for specialists with scale, sourcing capability and omni-channel reach.

Market Opportunity and Expansion

£700 million

Current UK tile market

£2.1 billion

Total addressable market

including adhesives, tools, splashbacks and large format panels.

"Through our sourcing expertise, digital reach and trusted brands, we are well-positioned to capture share in adjacent categories and increase wallet share from trade and homeowner customers alike."

Category Expansion

Through expanding our offer into adjacent categories we are able to significantly expand our addressable market and provide hard surface covering solutions across more of the house.

Driving Growth Through Adjacent Categories

Luxury Vinyl Tiles

Market size = £285m

Current sales = £4m

5% share = £14m

Opportunity = £10m

Shower Panels

Market size = £100m

Current sales = £1m

5% share = £5m

Opportunity = £4m

Outdoor Tiles

Market size = £160m

Current sales = £6m

10% share = £16m

Opportunity = £10m

Wood & Laminate

Market size = £285m

5% share = £14m

Opportunity = £14m

Splashbacks

Market size = £50m

5% share = £2.5m

Opportunity = £2.5m

XXL Porcelain

Market size = £120m

10% share = £6m

Opportunity = £6m

Porcelain and ceramic tiles are some of the most versatile options for walls and floors around the home. Porcelain is dense, water resistant and hard wearing, making it well suited to kitchens, bathrooms and high traffic areas. Ceramic is lighter and easier to cut, which makes it a good fit for living spaces and wall tiling. Both types are available in a wide range of sizes, colours and finishes, from soft matt styles to more detailed natural stone, wood and patterned designs. Easy to maintain and long lasting, they’re a simple way to bring texture and colour into the home.

Outdoor 2cm tiles are built for patios, paths and garden areas, with the thickness and strength to handle weather changes and heavy foot traffic. The extra depth gives them added stability, while the slip-resistant surface helps keep things safe underfoot. They come in a choice of stone and concrete looks, with finishes that create a clean, modern feel outside. It’s a low-maintenance way to get a smart, durable surface that holds up year-round.

Natural stone tiles bring a more individual look to floors and walls, with natural variation in colour, pattern and texture across every tile. Available in materials like marble, slate, limestone and travertine, each one shows unique markings and tonal shifts that add character to any space. They are well suited to kitchens, bathrooms, hallways and living areas, offering a durable surface that works well in both classic and modern interiors. The range includes different sizes and finishes, making it easier to get the right fit for the job.

Porcelain shower trays are made for everyday use, with a surface that’s easy to clean and resistant to stains and scratches. They sit well alongside tiled walls and floors and blend in with the overall look. Each tray has a built-in gradient that helps water drain efficiently, making them a reliable choice for walk-in showers and wet room setups.

Luxury Vinyl Tile flooring combines style and durability with its wide variety of finishes, from rustic wood grains to realistic stone.

All vinyl flooring tiles are designed with a hardwearing and stain-resistant wear layer, making them easy to clean and maintain, and our Pronto range is also water-resistant and moderately slip-resistant so it is stylish with safety in mind.

LVT is compatible with water-based underfloor heating systems, providing an extra source of warmth and comfort in living spaces.

Seamless, waterproof wall shower panels create a low-maintenance finish and a luxurious look for a floor-to-ceiling look in the bathroom, in porcelain or laminate.

Extra large tiles create a smooth, open feel that helps make any room appear more spacious. With fewer grout lines, they give walls and floors a clean look that’s easy to maintain. Available in a variety of finishes including stone and marble effects, they’re a great choice for kitchens, bathrooms and open plan areas where a refined style works well.

Wood and laminate flooring bring a natural look and warm feel to your home, with finishes that suit everything from traditional to modern spaces. Laminate offers the appearance of real wood but is designed to be more durable and easier to care for. It’s a great choice for busy rooms like hallways and living areas, where you need a floor that’s practical but still looks the part.

Glass and metal splashbacks offer a clean, practical solution for protecting kitchen and utility walls. They are easy to wipe down and resistant to heat and stains, making them ideal for areas behind hobs and sinks. With a choice of colours, finishes and patterns, splashbacks can highlight key areas or tie in with the rest of your space, all while keeping maintenance simple.

Porcelain splashbacks offer a tough, low-maintenance surface for busy kitchen spaces. They’re resistant to heat, stains and moisture, making them a practical choice for protecting walls behind cookers and sinks. Available in a range of styles, from stone to patterned designs, they can bring texture and colour into your kitchen without the need for grout or complicated upkeep.

Designed to recreate the look of slat wood panelling with the added benefit of sound-insulating properties, decorative wood wall panels are available in various wood tones to suit every aesthetic. Suitable for use in a variety of rooms including living rooms, bedrooms, kitchens, hallways and other spaces, they are simple to install, offering maximum design impact and requiring minimal effort. Designed with longevity in mind, they help retain the natural finish of the wood, while the strong backing foam provides up to 60% noise reduction.

Balance Exposure Across Residential and Commercial

60%

of our sales are linked

to domestic RMI, underpinned by resilient home improvement spend.

40%

of our sales are

in commercial projects, infrastructure and new-build housing.

"Our size, scale and exclusive product ranges enable us to bridge both professional trade and homeowner segments, while our multi-brand model allows targeted propositions across each channel."

The UK tile market splits into two broad sectors – the residential repairs, maintenance and improvement (‘RMI’) sector, accounting for around 57% of the market, and the commercial and housebuilder sector, accounting for the remaining 43% (source: AMA/Barbour AMI Research). The commercial market includes all types of commercial building projects, including infrastructure, as well as new-build residential property, including housebuilding. Within Topps Group, Topps Tiles is mainly focused on the residential RMI market, although it also sells into the commercial sector through its trade customers, Tile Warehouse is largely focused on the residential RMI market, Parkside is focused on the commercial market, Pro Tiler Tools serves trade customers and contractors who may be working across either or both of these markets and CTD sells into both sectors, including into the housebuilder market, a sector not previously served by Topps Group.

An external survey of the tile market is published by AMA Research. It covers the whole of the UK tile market, based on manufacturer and supplier data. The most recent report, dated May 2025, estimates the size of the UK tile market in 2024 at £418 million, measured at manufacturers’ selling prices (‘MSP’), this is 1% higher than the estimate for 2023 (£414 million at MSP). Based on the available data, when converted to customer selling prices, the Group estimates the UK tile market across the domestic and commercial sectors to be in the region of £700 million annually. Following the strategic expansion into a wider range of hard surface product categories, the Group estimates its addressable market to be around £2.1 billion per annum. These additional categories include product areas such as luxury vinyl tiles, wood, splashbacks and shower panels.

The domestic tile market is large and offers long-term potential – of the approximately 30 million dwellings in the UK, the average age is around 70 years, giving a significant and growing need for repair, maintenance and improvement spend. Of the 24.4 million homes in England, 15.8 million were owner occupied, 4.6 million were private rented, and 4.0 million were social rented (either from housing associations or local authorities (source: 2022-23 English Housing Survey, DLUHC).

Following the Covid-19 pandemic in 2020, the UK home improvement market was buoyant across the following two years of 2021 and 2022. This was the result of a number of factors being particularly favourable for the domestic market, including people spending more time in their homes while at the same time having restricted choices for their economic activity, a boost to housing prices and transactions through reduced stamp duty and low interest rates, and substantial excess savings built up through the Covid-19 lockdown period.

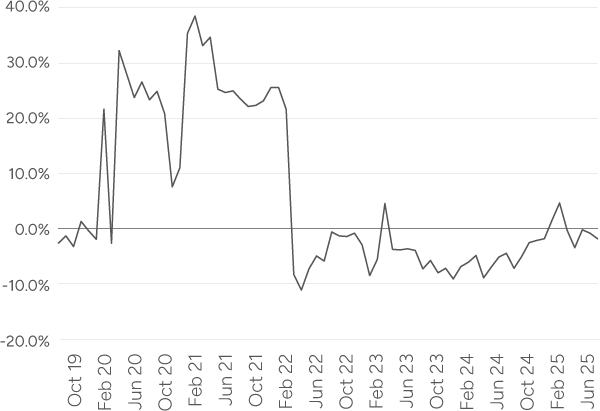

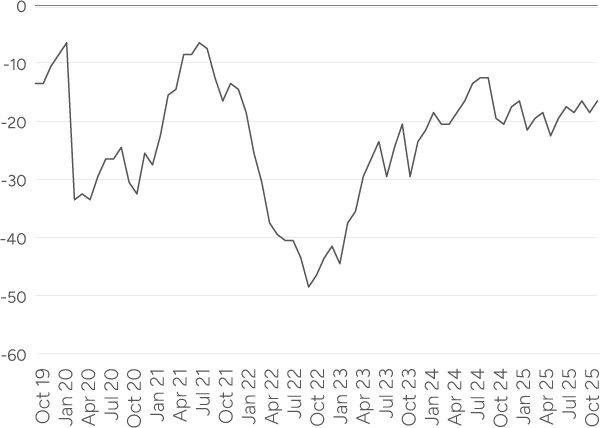

However, from 2023 onwards, a number of adverse market factors have increasingly weighed on sentiment. Consumer confidence over recent years has been consistently negative, averaging -34 over the FY23 financial year and -19 for the FY24 financial year (source: GFK). In the FY25 financial year the index was flat year on year at -19, reflecting the stagnant nature of consumer spending.

The Barclays UK consumer spending report breaks down spending across a number of categories, including the home improvement and DIY category. Following a 7.2% average monthly year-on-year decline across the FY24 financial year, the index improved in the FY25 financial year but remains in decline of 2.2% (source: Barclays)

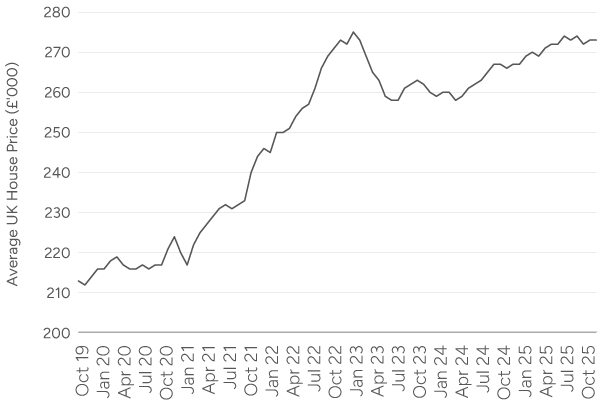

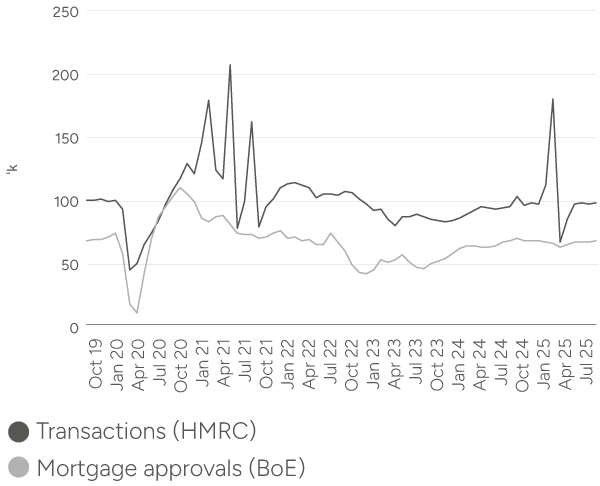

The UK housing market is a useful indicator of the market. In a market of rising prices, homeowners tend to feel more affluent and are more confident in spending money on their homes. Following a modest increase in the average price of a house in FY24 of 0.5%, in FY25 average house prices grew by 3.3% and ended the year with growth of 2.1% in September 2025 (source: Nationwide). Mortgage approvals and housing transactions also impact the level of demand on home improvement projects, albeit with a lag. Mortgage approvals rose 10.7% in the FY25 financial year compared to FY24; however, this strong performance was driven between the months of October 2024 to January 2025, over the second half of FY25 approvals were 2.0% higher than the prior year (source: Bank of England).

The UK commercial tile market is highly fragmented and regionalised with only a small number of scale competitors. The smaller competitors tend to specialise in certain sectors of the market – examples being transport, restaurants, automotive, leisure, offices or higher-end residential.

The Group’s success in this market results from appealing to both designers and architects, with our quality and differentiated offer, and to contractors, who may require larger quantities of products, in short timescales. The Parkside business is able to service both categories: it can leverage its access to differentiated product through the Group’s supplier relationships, as well as its buying advantage and stock-holding position to support volume sales.

Total construction output for the new-build private commercial work across all product types decreased by 7.4% year on year on a volume, seasonally adjusted basis (FY24: decreased by 1.5%) (source: ONS).

UK House Prices

Source: Nationwide

Consumer Confidence

Source: GfK

Construction Market Size

Source: ONS

Mortgage approvals & housing transactions

Source: Bank of England and HMRC

UK Consumer Spending Report – Home Improvement DIY Spend (YoY)

Source: Barclays